Video 1

Commodity money is a good that functions as money through exchanges. Representative money is when money is backed up by a metal such as silver or gold. Fiat money is not backed by metal and backed up by the government's word. Money has many functions as well such as being a medium of exchange, store of value, and a unit of account.

Video 2

In mm graphs, Demand slopes downward as it did in the S and D graphs because price and demand have an inverse relationship. Certain factors that can shift the Demand is if there was an incentive to want more money via loans and etc. If people borrowing and spending more money, then the Demand will shift right. In effect it would put upward pressure on the interest rate. If the Fed wants to lower the interest rates in certain times such as an recession, they would increase the money supply.

Video 3

The FED has expansionary and contractionary policies. In expansionary, the reserve requirement (RR) decreases, the discount rate decreases, and the FED buys bonds to expand the money supply. A way to remember this is "buy bonds = big bucks!" In contractionary, the reserve requirement increases, the discount rate increases, and the FED sells bonds to lower the money supply.

Video 4

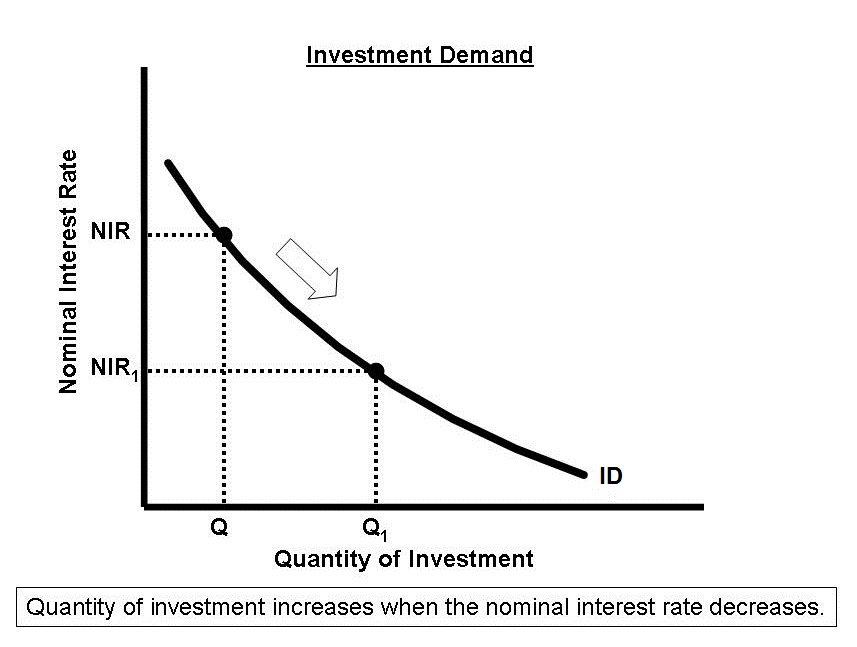

On the loanable funds graph has the same axes as the Money Market graphs. Demand for loadable funds is downward sloping because when interest rates are lower, people demand more money and vice versa. Supply is upward sloping and it also dependent on savings.Savings is a positive factor in this market because the more people save, the more banks will have available. In order to shift the Supply curve left or right there must be an incentive or an lack of a incentive for people to save. The money market and loanable funds are connected, loanable funds is the source of money for the money market.

Video 5

Banks create money by making loans. The formula for the money multiplier is 1 / reserve requirement. The money multiplier is then multiplied by the amount of money loaned to get the potential total amount of money created in the banking system. This can only be done by assuming that the banks have no excess reserves. If there are excess reserves, then the potential total amount of money is lower.

Video 6

The money market, loanable funds market, and AD/AS market have affects on each other, The money market is where the government gets the money, the demand for loans increase for another source of money(government spending), and the AD increases because government spending is a determinant for the AS/AD market. The equation of exchange is MV=PQ can be used to explain the relationship, as price levels increase the interest rates increase. This can be explained by the "fisher effect." It ultimately means that there is a 1:1 ratio.