Unit I

Macroeconomics Vs. Microeconomics

-Macroeconomics: The study of the economy as a whole.

“Looking at the big picture”

- Inflation, international trade, and wages

- Microeconomics: The study of individual or specific units of the economy.

“Looking at the trees but not the forest”

- Supplied and demand, Market structure: monopoly, competition

- Business organization: corporations

· Positive Economics Vs. Normative Economics

- Positive Economics: Attempts to describe the world as is.

“Fact based”

- It is very descriptive.

- It thrives on "what is"

- Collects and presents facts

- Example: Oil dropped in price from $3.00 to $2.00 in the past month.

- Example: Oil dropped in price from $3.00 to $2.00 in the past month.

- Normative Economics: Attempts to describe the world should be.

“Opinion based”

- The national minimum wage should be raised.

· Needs Vs. Wants

- Needs: Basic requirements for survival.

- Example: food, shelter, water, and clothing

- Wants: Desires of citizens.

“You don’t need it but you still want it”

· Goods Vs. Services

- Goods: tangible commodities.

“Something you can feel or touch”

-Capital goods: Items used in the creation of other goods.

-Example: tires, windows on a car, etc.

-Consumer goods: Goods that are intended for final use by the consumer.

- Services: Work that is performed for someone.

-Example: restaurant, barber shop, etc.

· Scarcity Vs. Shortage

- Scarcity: The most fundamental economic problem that all societies face.

- How to satisfy unlimited wants with limited resources.

-Example: Oil

- Shortage: Quantity demanded is greater than the quantity supply.

· Factors of Production:

1. Capital: 2 types(Human and Physical)

- Human capital: Knowledge, skills, abilities, and talents that are gained through education and work experience.

- Physical capital: Tools, machines, and robots.

2. Entrepreneurship (innovative risk taker)

3. Land: natural resources

4. Labor: The work force

· Trade Off: Alternatives that we give up when we choice one course of action over another.

· Opportunity Cost: Next best alternative

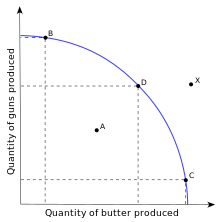

- 4 Assumptions

- Two goods

- Fixed resources(land, labor, capital, and entrepreneurship)

- Fixed technology

- Full employment of resources

-Attainable but inefficient

-UnderutilizationPoints B, C, and D: On the curve

-Attainable and efficientPoint X: Outside the curve

-Unattainable3 Types of Movement that occur within the PPC:

1. Inside the Curve

-Occurs when resources are underemployed or unemployed.

2. Along the PPC

3. Shifts of the PPCWhat causes the PPC/PPT to shift?

1. Technological changes

2. Economic growth

3. Change in resources

4. Change in the labor force

5. Natural diseases/war/famine

6. More education and training(human capital)

Elastic demand: Very sensitive to a change in price, (E>1), product is not a necessity, and there are available substitutes.

- Examples: Soda, steaks, candy, and fur-coats.

- Examples: Gas, salt, milk, insulin, medicine, and toothpaste.

Price Elasticity of Demand(PED):

- Step 1: Quantity=(New quantity-old quantity)/old quantity

- Step 2: Price=(New price-old price)/old price

- Step 3: % change in quantity demanded/ % change in price

Total Revenue: The total amount of money a firm receives from selling goods and services.

Marginal Cost: Cost producing one more unit of a good.

Formulas:

- Price * Quantity = Total Revenue

- Rent, mortgage, insurance, and salaries.

Marginal Cost: Cost producing one more unit of a good.

Formulas:

- TFC + TVC = TC

- AFC + AVC = ATC

- TFC / Q = AFC

- TVC / Q = AVC

- TC / Q = ATC

- TFC = AFC * Q

- TVC = AVC * Q

- MC = NTC-OTC

Demand: The quantities that people are willing and able to buy at various prices.

Supply: The quantities that producers or sellers are willing and able to produce at various prices.

Supply: The quantities that producers or sellers are willing and able to produce at various prices.

- The Law of Demand: States there is an inverse relationship between price and quantity demanded (As price decreases, quantity decreases) and (As price decreases, quantity increases).

- A "change in quantity demanded" is caused by a change in price.

- A "change in demand" is caused by

- Change in buyer's taste (advertisement)

- Change in the # of buyers (population)

- Change in income (normal goods and inferior goods)

- Change in the price of related goods (complementary goods and substitute goods)

- Change in expectations

- The Law of Supply: States there is a direct relationship between price and quantity supplied (As price increases, quantity increases) and (As prices decreases, quantity decreases).

- A "change in quantity supplied" causes a change in supply.

- A "change in supply" is caused by

- Change in weather

- Change in the # of suppliers/sellers

- Change in technology

- Change in taxes or subsidies

- Change in the costs of production

- Change in expectations

Supply Curve Shifts to the Left:

- Increase in cost of production

- Decrease in technology

- Increase in taxes

- Decrease in subsidies

- Decrease in # of sellers

- Decrease in weather

Supply Curve Shifts to the Right:

- Decrease in cost of production

- Increase in technology

- Decrease in taxes

- Increase in subsidies

- Increase in # of sellers

- Increase in weather

Equilibrium: The point at which the supply curve and the demand curve intersect. At this point, all resources are being efficiently used.

- Excess demand occurs when the quantity demanded is greater than the quantity supplied. This will result in shortages, where consumers cannot get the quantities of items that they desire.

- Price ceiling creates a shortage. A price ceiling occurs when the government puts a legal limit on how high the price of a product can be. In order for a price ceiling to be effective, it must be set below equilibrium. For example, the government sets a price ceiling on flu shots and shots are sold for less than what they are worth; therefore creating a shortage of flu shots.

- Ex: Rent control (New York & San Francisco)

- Excess supply occurs when the quantity supplied is greater than he quantity demanded. This will result in a surplus, where producers have inventories they cannot get rid of.

- Price floor is the lowest legal price a commodity can be sold at. A price floor creates a surplus. Price floors are used by the government to prevent prices from being too low. The most common price floor is the minimum wage.

Business Cycle Terms:

- Peak: Highest point of real GDP.

- Greatest amount of spending and lowest amount of unemployment.

- Inflation becomes a problem in this phase.

- Expansion(Recovery Phase): Real GDP is increasing due to an increase in spending and a decrease in unemployment.

- Contraction/Recession: Real GDP declines for six months due to a reduction in spending and increasing unemployment.

- Trough: Lowest point of real GDP.

- Least amount of spending and highest unemployment.

No comments:

Post a Comment